A cleaner drug, zero competition, and two binary readouts this year. Plus, Powell and oil near $99.

Three straight losing weeks for the S&P. Oil within spitting distance of $99. Jerome Powell steps to the mic on Wednesday. Jensen Huang kicks off Nvidia’s GTC today. Happy Monday.

The S&P 500 closed Friday at 6,632, down 1.6% on the week and roughly 5% off its January high. Dow at 46,558. Nasdaq at 22,105. Gold above $5,100 an ounce. WTI crude at $98.71. Every member of the Mag 7 is red on the year.

The oil picture keeps getting worse, not better. Bloomberg modeled Strait of Hormuz shutdown scenarios this week: one month puts crude around $105, two months at $140, three months at $165. The Trump administration suspended the Jones Act to try to tame prices. None of it has been enough.

Goldman put a number on the inflation risk: a $10 sustained oil price increase would push year-over-year headline CPI from 2.4% to roughly 3.2% within three months. That’s the backdrop walking into Wednesday’s FOMC decision.

In a tape this messy, the names worth watching are the ones where the catalyst is specific, the timeline is known, and the thesis doesn’t depend on the Fed saying the right words. This week’s research briefing is one of those.

The company.

Edgewise Therapeutics (NASDAQ:EWTX) is a clinical-stage biotech out of Boulder, Colorado. $3.1 billion market cap. $530 million in cash. Two drugs, each with a real shot at rewriting their respective markets.

The stock has roughly tripled from its 52-week low of $10.60 and closed Friday at $29.59. Two major data readouts are coming this year.

The heart drug: why the mechanism matters.

According to independent research shared with WOLF Financial, existing drugs for hypertrophic cardiomyopathy (HCM) essentially work the same way. Bristol Myers Squibb’s Camzyos and Alnylam’s Myqorzo both suppress the heart’s pumping action to reduce dangerous pressure buildup.

They work. Camzyos did $1.07 billion in sales last year.

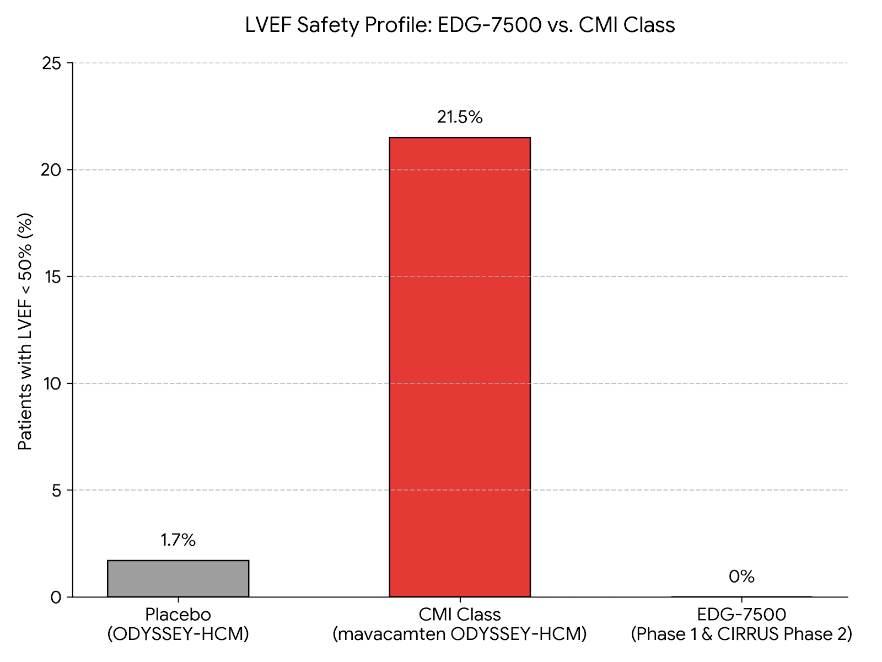

But they carry a serious liability: they can suppress the pumping function too much. In the Phase 3 ODYSSEY-HCM trial for non-obstructive HCM, 21.5% of patients on Camzyos saw their ejection fraction (the percentage of blood the heart pumps each beat) drop below 50%. On placebo, just 1.7%. That earned the drug class a boxed warning for heart failure.

EDG-7500 takes a different approach. Instead of suppressing the pump, it helps the heart relax between beats. In non-obstructive HCM, that’s the actual problem. The heart can’t relax properly. Existing drugs are solving the wrong problem in those patients.

The safety comparison tells the story at a glance.

Across 72 Phase 1 subjects and all Phase 2 participants, zero patients on EDG-7500 saw their ejection fraction drop below 50%. No correlation between drug concentration and heart function across a 60-fold exposure range. Compare that to the 21.5% rate for the existing drug class.

The CIRRUS Part D full efficacy readout is expected by June 2026, covering 12-week endpoints across more than 40 patients in both obstructive and non-obstructive HCM. A safety-only interim last December (over 2,600 patient-days of monitoring without incident) moved the stock 21% in a single session. That was just safety data. The efficacy numbers are the real test.

The other drug: a disease with zero treatments.

Research shared with our team points to Edgewise’s second program as perhaps the bigger story.

Sevasemten is being tested in GRAND CANYON, a global pivotal trial across 175 adults with Becker Muscular Dystrophy (BMD) in 12 countries. There are currently zero approved treatments for this disease. None.

A positive readout, expected Q4 2026, would make Sevasemten the first-ever FDA-approved therapy for BMD. The agency confirmed in a 2025 meeting that a positive GRAND CANYON result would be sufficient as a single pivotal study for traditional approval, with an NDA filing targeted for H1 2027.

The preview data is hard to ignore.

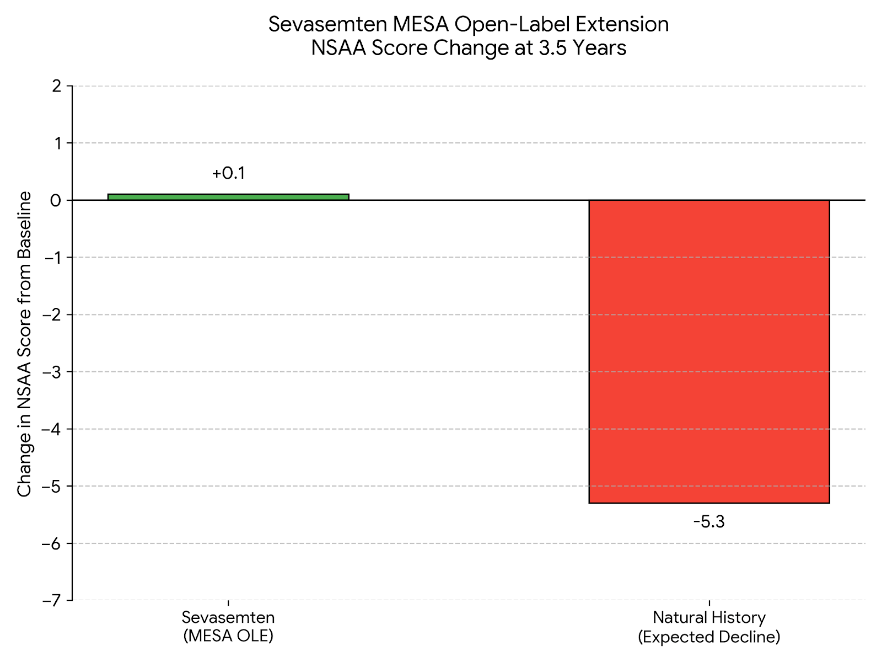

Over 3.5 years of open-label extension data, treated patients maintained essentially stable mobility scores (+0.1 point improvement). Untreated patients typically decline by about 5.3 points over the same period. The company says the trial is powered at over 98% to detect statistical significance.

The flow.

Options flow data shows a notable position still open from January 7: 2,000 August 25/36 call spreads bought at $3.20, a roughly $640,000 bullish bet. The timing and structure suggest this isn’t a near-term play. More likely positioning for the GRAND CANYON readout or a potential acquisition scenario.

The short interest adds another layer. 15.6% of the float is sold short with more than 8 days to cover. A positive data outcome wouldn’t just be a fundamental repricing. That short structure could mechanically amplify the move.

What to watch.

Today, Wedbush hosts a key opinion leader call featuring Dr. Daniele Massera from NYU Langone’s HCM Program, which follows more than 3,000 HCM patients. This is a positioning event, not a trading event. It builds institutional conviction ahead of the CIRRUS data in June and the GRAND CANYON readout in Q4.

The stock’s RSI sits around 52, roughly neutral. Support in the $27-28 range, recent highs around $31-32.

Two separate binary catalysts. A cleaner safety profile than anything else in the drug class. A disease with no approved treatments and a Phase 3 readout later this year. That’s the setup.

Thanks for reading! For more updates throughout the week, follow @WOLF_Financial on X.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

Login to comment