Gold was supposed to be the crisis trade. It isn’t.

Instead of rallying on war, gold is having its worst month since February 1983 — down 17% in March as the Iran conflict does something no one expected: it is killing the Fed easing thesis that had kept gold prices elevated for months.

And gold mining stocks are now paying the full price.

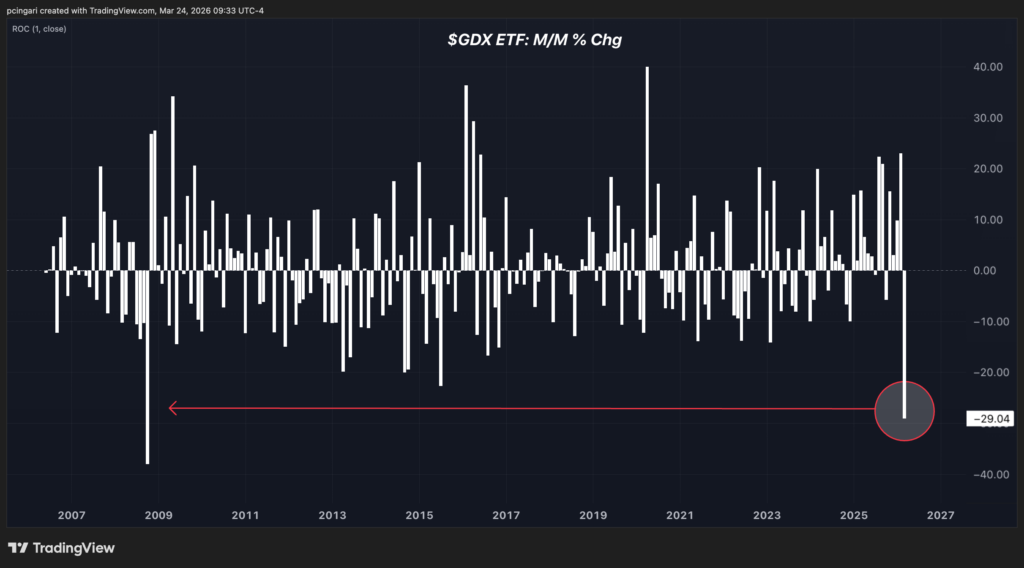

The VanEck Gold Miners ETF (NYSE:GDX) has collapsed nearly 29% this month — the fund’s worst performance since October 2008, the month after the Lehman collapse.

The Yield Shock Behind The Gold’s Collapse

The mechanism is not complicated, but it is brutal.

U.S. 10-year real yields — the spread between nominal Treasury yields and the breakeven inflation rate, and the most direct measure of the opportunity cost of holding gold — have surged 37 basis points month-to-date.

That is the largest monthly spike since September 2022.

Gold pays no coupon. When real yields rise this fast, the gold’s investment thesis worsens.

The Iran war, rather than suppressing yields through a flight to Treasuries, has done the exact opposite: it has reignited inflation expectations.

Elevated oil prices from the risk of a disruption in the Strait of Hormuz feed directly into input costs and inflation projections.

The market’s conclusion is no longer that the Fed should cut rates to protect growth. It is that rates cannot be cut at all because inflation is back, and the risk of a hike is quietly rising.

The Fed Is Trapped — And Markets Know It

Prediction markets are boxing the Federal Reserve into a corner — in real time.

On Polymarket, the probability of no policy change at the April 28–29 FOMC meeting has surged to 94.85%, up 13.5 percentage points in just one week.

But the bigger shift is in the 2026 rate path.

Markets now assign a 31% probability to zero rate cuts this year — the single most likely outcome, marking a sharp reversal from expectations of two to three cuts at the start of 2026.

That prior base case is quickly unraveling. The probability of exactly two cuts has fallen to 18.5%.

Meanwhile, what was once dismissed as a tail risk is moving into the core distribution: markets now price a 19.5% chance of at least one rate hike in 2026.

The Miner Bloodbath In Context

GDX’s 29% collapse in a single month is a data point that requires historical framing.

October 2008 — the previous comparable drawdown — was the month global credit froze.

The current selloff is happening in a functioning credit market, which makes it more about the structural repricing of gold’s macro justification than about systemic panic.

Gold miners run with operational leverage. When gold was pricing in three or four Fed cuts in 2026, the mines were profitable futures factories.

Now, with gold down 17% and cost structures under pressure (energy, a major mining input, has been pushed higher by the same Iran conflict that has provided the geopolitical headline), the leverage has inverted.

The same war that gave gold its narrative is making it operationally more expensive to mine.

The Market Read

This gold movement has two live wires.

If real yields stabilize or reverse — through a Gulf ceasefire, a sharper-than-expected economic slowdown, or a Fed pivot signal — gold’s 17% monthly drop has the structure of a violent snap-back candidate.

Moves of this magnitude have occurred only a handful of times in modern market history.

Repricing events of this speed tend to reverse with equal force.

But if the inflation signal from the Iran disruption embeds structurally into CPI — if oil stays elevated, input costs compound, and the Fed remains frozen — then the 1983 parallel stops being a comparison and becomes a floor.

Real yields stay high, the easing thesis stays dead, and the miners face a prolonged earnings reset with no obvious catalyst for recovery.

Photo: Shutterstock

Login to comment