This week’s Wolf Pick: FirstCash Holdings (FCFS)

A 40% spike in oil prices has done something no pawnbroker marketing budget ever could. It made tax refund season profitable for the pawn shop.

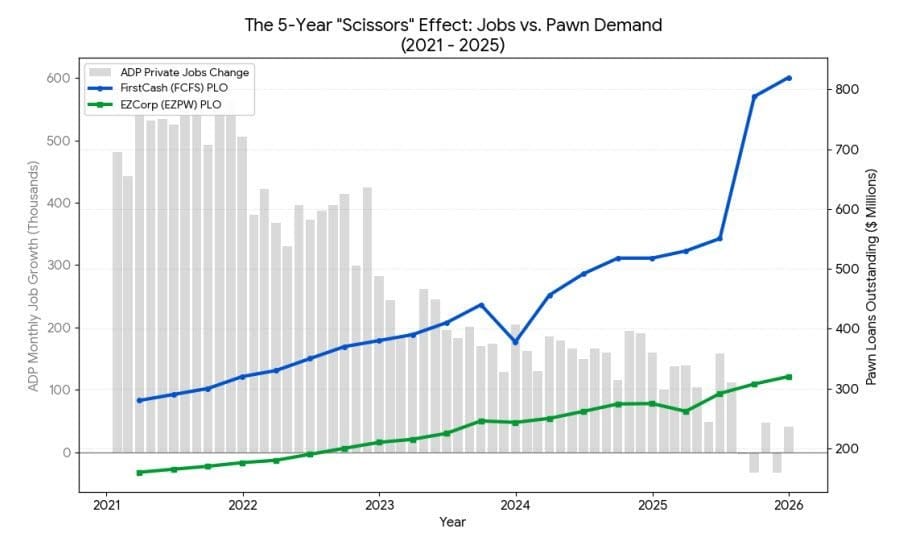

This week’s Wolf Pick looks at FirstCash Holdings (NASDAQ:FCFS), a $8.4 billion operator of more than 3,000 pawn stores across the U.S., Latin America, and the U.K., and why the Iran conflict may have structurally broken the seasonal model that Wall Street has used to forecast this business for a decade.

The seasonal playbook, broken

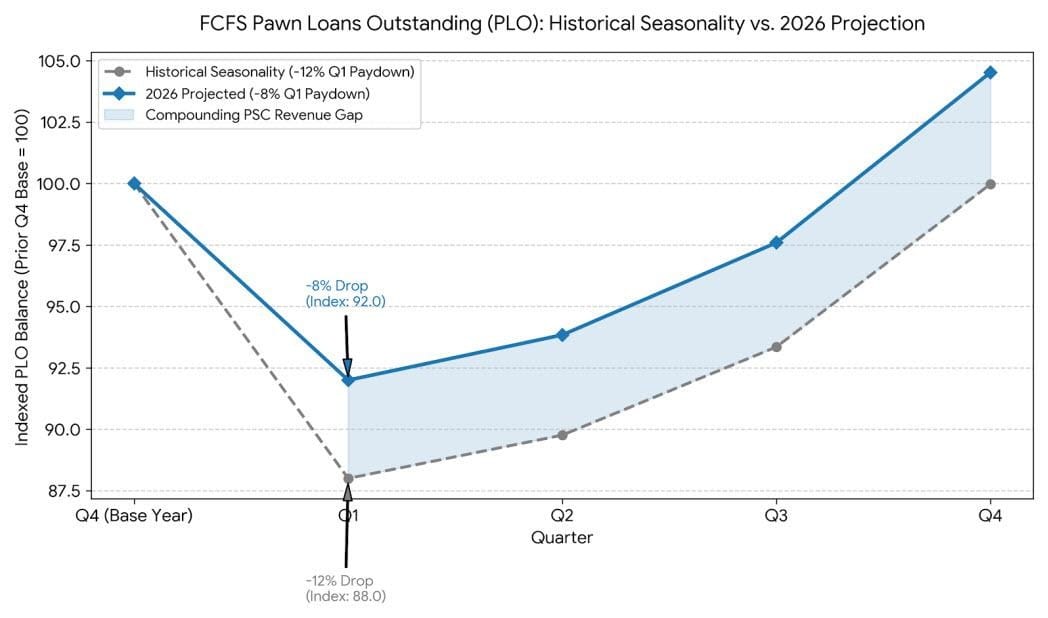

Here’s how pawn lending is supposed to work in Q1. Tax refunds arrive. Consumers walk in, redeem their pawned jewelry, and pawn loan balances (called PLO, or Pawn Loans Outstanding) roll off. The historical median Q1 paydown is about 12%. Analysts model for this. It’s as reliable as the calendar.

The problem: that refund money has somewhere else to go this year.

According to independent research shared with Wolf Financial, Americans collectively spend roughly $350 billion on gasoline annually under normal conditions. With WTI crude above $100 and Brent pushing $115 on the back of the Strait of Hormuz closure, a 40%-plus oil spike translates to approximately $140 billion in incremental pump spending absorbed in a single year. That’s money that was previously available for debt paydown, discretionary purchases, or redeeming pawned collateral. The tax refund check clears and goes directly into the gas tank.

The downstream effect on FCFS is mechanical. Consumers who would ordinarily redeem their pawned items don’t have the cash. The loan stays active longer, and pawn service charge (PSC) fee income runs hotter. At the same time, customers squeezed between elevated energy costs, persistent food inflation, and flat wage growth are originating new pawn loans in a quarter when they’d normally be redeeming old ones. FCFS is collecting fees from both sides of the cycle.

Current consensus models approximately an 8% Q1 paydown. That 400-basis-point gap from historical norms sounds small. In pawn lending, it’s enormous. PLO balances aren’t just a snapshot of today’s revenue. They’re a leading indicator for fee income over the next one to three quarters, because PSC fees accrue on outstanding principal over the life of the loan. If balances run 400 basis points higher than modeled through Q1 and Q2, that elevated base generates compounding fee income into the back half of 2026. Consensus Q3 and Q4 estimates are currently being set off a Q1 reset that isn’t happening.

The accidental upgrade

There’s a second angle here that’s getting almost no attention. When FirstCash acquired American First Finance (AFF) in 2021, a lease-to-own and point-of-sale financing platform for subprime consumers, the market punished the stock. The logic was straightforward: FCFS had just taken on subprime consumer lending risk right as the Fed was telegraphing its most aggressive tightening cycle in four decades.

Research reviewed by Wolf Financial suggests the opposite is playing out. The consensus risk model for AFF assumes its borrower base consists of chronic subprime consumers whose default rates track unemployment. What that model misses is what happens during credit tightening. When JPMorgan and Citigroup tighten their credit boxes (and both have explicitly signaled they’re doing so), consumers who previously qualified for standard revolving credit get rejected and slide down the access ladder. These aren’t serial defaulters. They’re structurally safer, higher-repayment borrowers displaced from the prime market by circumstance. They show up at AFF needing to finance a $600 tire replacement, and AFF onboards them at its standard high-yield rates. Borrower quality is quietly improving while the yield stays constant.

The data backs it up. In early 2025, when consensus modeled a spike in AFF default rates, lease and loan loss provisions actually fell 13% year over year.

The gold margin of safety

One more structural point. FCFS lends against gold collateral using internal pricing tables based on $3,000 per ounce. Spot gold closed Friday ~$4,550. Their entire gold collateral book is carried at roughly a 34% discount to market value.

A research note reviewed by our editorial team highlighted that a $500 loan on a $1,000 item has 140%-plus collateral coverage at current spot prices. The practical implication: the supposed downside scenario, a severe economic contraction that drives forfeitures higher, is actually a profit event. More forfeitures means more gold scrapped at a massive premium to book cost. The bear case and the bull case for FCFS’s gold book have converged.

What to watch

FCFS reports Q1 earnings on April 30. The number to focus on is the Q1 PLO paydown rate. If it comes in materially shallower than the consensus -8%, the revision cycle for the rest of 2026 starts immediately. Beyond earnings, watch for any signals from management on AFF loss provisions and same-store pawn origination trends.

Thanks for reading! For more updates throughout the week, follow @WOLF_Financial on X.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

Login to comment