Amkor Technology, Inc. (NASDAQ:AMKR) has what I would consider a very fascinating long-term story, but in the near-term, it's a bit uncomfortable. That is primarily because of its current share price, not the business itself. The business has a lot going for it, and I'll drill down into those later. The price, though, is not as cheap as it looks, in my opinion, and that is because the market is already valuing the upside from the company's Arizona campus. That facility is not going to reach meaningful production levels until 2028, according to what Amkor tells us.

I believe that paying 14x EV/EBITDA for a business that is going to have sharply negative free cash flow, smaller gross margins, and very high capex figures over the next two fiscal years doesn't sound like the best possible deal. To be clear, I'm confident in Amkor's growth and expansion over a longer period of 5-10 years, but the next two years are also important when deciding what the stock is worth now.

Amkor's Business

I think it's fair to say that most people who own a smartphone, a laptop, or a car have interacted with Amkor's work on some level, even if they don't know it. The company runs one of the biggest outsourced semiconductor assembly and test provider (OSAT) businesses in the world, along with ASE Technology Holding Co Ltd (NYSE:ASX). OSAT companies are a critical part of the semiconductor supply chain, and they handle the packaging, testing, and prep work for semiconductor chips before they go into the devices I mentioned above.

There are a fair few tailwinds for the company's business today because of how complex chip design and packaging have now become. For example, Nvidia Corp (NASDAQ:NVDA)'s AI accelerators depend on high-bandwidth memory connected through exactly this kind of advanced packaging architecture. We can also say the same for Apple Inc. (NASDAQ:AAPL)‘s entire lineup of custom silicon.

Also, Amkor's product mix is interesting to me because of how much of its revenue comes from just one segment, and that segment has what I'd consider to be some of the strongest possible industrial support in the company's sector. Advanced Products (the segment that contains its flip-chip chip-scale packages, flip chip ball grid array, and memory and wafer-level packages) brought in around 83% of its revenue in FY25, and it only has a few big customers that are driving sales here. According to the same FY25 annual report, Apple is Amkor's biggest customer (~30% of total revenue), and it's not even close. Then there's Qualcomm Inc (NASDAQ:QCOM), which made up another 11% of the total for the year. Together, those two companies are supporting 40% of Amkor's sales, and they are two of the biggest chip designers and producers globally. Besides them, there are some other AI-adjacent hyperscalers, so that's an incredibly solid customer base that's not going anywhere anytime soon.

I also believe that Amkor's geographical location is another strategic advantage, especially when you look at the current geopolitical landscape. Generally speaking, most of the advanced packaging industry is in Asia, especially in Taiwan and China. ASE Technology, which is arguably the biggest of them, is in Taiwan, and JCET Group is a Chinese company. Amkor is the only one of them that has its headquarters in the US, and that's partly why it is able to take advantage of CHIPS Act funding support for its $7 billion Arizona facility and have Apple and Nvidia as anchor customers there.

The Bull Case: Arizona And The AI Packaging Cycle

In my intro, I mentioned that I can see the long-term appeal to owning Amkor stock, and the Arizona campus is the main reason why. The company is spending $7 billion to build what will be the most advanced semiconductor packaging facility in the US, and it is supposed to start production there in early 2028. Roughly 5-8% of that amount could come from the US government's CHIPS Act purse if Amkor takes the initial $400 million in direct funding and another $200 million in loans from the program, so it will fund the rest of the build by other means.

All of that is normal, but the main reason why I'm ascribing so much value to the campus is how important it is in terms of a geopolitical advantage. The US has made the semiconductor industry and its domestic advanced packaging capacity a national priority, and that's not going to change anytime soon, regardless of which administration is in power. Amkor is the only company that can benefit from the policy change on such a huge scale, and that just gives it another moat.

Now, the demand backdrop for what Arizona will produce is as strong as anything I can point to in the semiconductor space. AI infrastructure buildout is as strong as it's ever been: all the hyperscalers are spending hundreds of billions of dollars on the data centers and other infrastructure that they will need over the next few years. Obviously, this means that the demand for advanced packaging capability, especially the kind of high-density interconnect work that allows GPU dies to communicate with high-bandwidth memory at the speeds modern inference and training workloads require, is going to increase pretty dramatically over the same period.

For context, Amazon, Meta, Google, and Microsoft are spending around $650 billion on AI-related infrastructure in 2026, and that is well over the ~$400 billion they spent on it in 2025. The outlook is pretty much in the same trajectory over the next few years, so Amkor is putting itself in a fantastic position to benefit from the buckets of money that are going around in the same period. The Arizona build is just one part of the story, though, and it's more of a future revenue expander than something we can account for presently.

I must highlight the fact that Amkor's existing business is already benefiting from the AI tailwinds today, and we can see this with its end markets. Communications, for example, covers a large part of Apple-driven demand, and it brought in 46% of the company's sales in FY25. Computing, which is where we can find the more AI-adjacent workloads, has gone from 16% of the total in FY23 to 20% in FY25. Also, Advanced Products (the segment) reached $5.6 billion in sales in the same year, and I expect that number to keep rising because of how quickly the company is moving toward the more complex, higher-margin work.

Now, the last thing I want to touch on here is Amkor's margins. We've seen its gross margin dropping steadily over the last few years after peaking in FY21 and FY22. FY25's number is around 14%, and a big part of that compression is how much the company is spending to build and improve its facilities when revenue isn't expanding just as quickly. I don't think that is going to change over the next two to three years, given how much Amkor is spending on the Arizona buildout, so it's another thing to keep in mind.

The Financials Show A Business With A Solid Foundation, But The Transition Will Be Painful

| Metric | FY2022 | FY2023 | FY2024 | FY2025 |

| Net Sales ($M) | $7,092 | $6,503 | $6,318 | $6,708 |

| YoY Growth | +16% | (8)% | (3)% | +6% |

| Gross Margin | 18.8% | 14.5% | 14.8% | 14.0% |

| Adj. EBITDA ($M) | $1,529 | $1,135 | $1,091 | $1,162 |

| EBITDA Margin | 21.6% | 17.5% | 17.3% | 17.3% |

| Diluted EPS | $3.11 | $1.46 | $1.43 | $1.51 |

| Operating Cash Flow ($M) | $1,099 | $1,270 | $1,089 | $1,096 |

| Free Cash Flow ($M) | $194 | $534 | $359 | $308 |

| Gross Capex ($M) | $905 | $750 | $744 | $905 |

| Net Cash ($M) | ~$300 | $390 | $488 | $546 |

I laid out the numbers in the table so we can get a solid picture of where this company has been over the last few years. I'd say that FY25 was a good year for Amkor's topline, primarily because it almost fully recovered from the semiconductor cycle downturn of 2023, and the momentum is strong enough that I'm confident about its long-term direction. Revenue was higher than in the prior two years, but that's the only metric that's actually higher. Everything else, from gross margins to EBITDA and cash flow, is trending in the opposite direction, and that is because of the Arizona facility build. Still, I think they're solid numbers, and they still look very attractive if one considers them in isolation.

The problem, though, is that we cannot evaluate Amkor in isolation, and the quarterly metrics are a more accurate representation of the company's performance.

| Metric | Q1 2025 | Q2 2025 | Q3 2025 | Q4 2025 | Q1 2026E |

| Net Sales ($M) | $1,320 | $1,510 | $1,987 | $1,888 | $1,600–1,700 |

| Gross Margin | 11.9% | 12.0% | 14.3% | 16.7% | 12.5–13.5% |

| Diluted EPS | $0.09 | $0.22 | $0.51 | $0.69 | $0.18–0.28 |

For example, the gross margins in Q1 and Q2 were lower than at any other point in the preceding eight quarters, and the EPS figures were almost negligible when compared to its recent history. Both metrics improved in the second half of the year, but we cannot ignore how volatile they are, especially when thinking about forward expectations. Look at the guidance we got from management for Q1 FY26: revenue between $1.6 and $1.7 billion, gross margin around 13%, and EPS of $0.18-0.28. Those are the lowest guided margin and EPS figures in the last three quarters, and in my view, they reflect typical Q1 seasonality and the early-stage cost absorption of the Arizona ramp. None of those things is going away anytime soon.

If we look at the free cash flow figures from FY25, you'll see that it is the lowest in the same 3-year period from FY23, at just over $300 million. But Amkor plans to spend ~$2.75 billion in capex in FY26, which is already 3 times higher than FY25's spend. So, if we assume that its operating cash flow stays at $1 billion for the year, I estimate that free cash flow will become sharply negative by the end of the year, somewhere between $1.7 and $1.8 billion. That's a huge swing, and it will be the same in FY27, before we see capex going back down to the expected level after Amkor completes the Arizona construction.

That's why I'm not excited about the stock at this time. Right now, with those figures baked in, investors will be funding a two-year trough in exchange for a facility that won't add anything to the topline until 2028. I understand the rationale, and I'm confident that it will be a big revenue multiplier when it finally comes online, but today's price is not exactly optimum for that trade, in my opinion.

Relative Valuation

| Company | EV/Sales (FWD) | EV/EBITDA (FWD) | P/E (TTM) | P/E (FWD) | Expected Revenue Growth |

|---|---|---|---|---|---|

| Amkor (AMKR) | ~2.4x | ~13.7x | ~48.6x | ~41.8x | 9% |

| ASE Technology (ASX) | ~3.0x | ~13.2x | ~52.0x | ~38.9x | 15% |

| KLA Corporation | ~18.0x | ~39.4x | ~52.8x | ~51.2x | 18% |

ASE Technology is the only directly comparable business to Amkor, but I included KLAC because it is also in the middle of the semiconductor supply chain.

Now, Amkor is trading at ~$73 per share, and all of its multiples in that table have fairly modest discounts to ASE. I think the discounts are easy to justify because ASE is a much bigger and more diversified company, and it has better growth prospects and margins, too. However, Amkor also has cheaper multiples than its sector medians, which tells us something. But that FCF gap that we expect this year is important, even if it is temporary.

I don't think it is reasonable to assume that Amkor's forward multiples can rise to the same level as ASE's, much less its sector medians, because its operating metrics are going to dip over the next two years. So the stock is essentially flatlining, and in my view, the only way to justify a more bullish outlook is if the company starts posting revenue growth near 20% over the same period. I don't see any catalysts for that happening, but it isn't something I can dismiss.

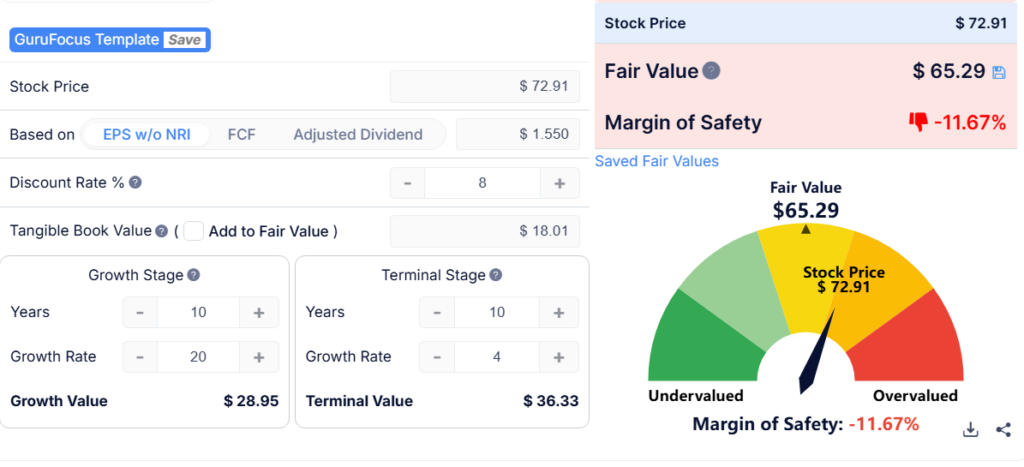

My DCF model gives me fairly similar figures to the multiples. For my base case, I'm assuming that the company can grow revenue at 15% annually for the next decade, including after the Arizona facility comes online. I'm also using a WACC of 8% and a terminal growth rate of 3%. With those figures, the stock's fair value is around $45, which is slightly higher than half of today's price.

My bull case, though, has sales growing at 20% over the same period, and the terminal growth rate goes up to 4%. That gives us a share price of $65. I think this is attainable, given all the advantages that the company already has going for it, but I don't think it is worth it over the next two years. If you model these same assumptions using FCF (which, as I've explained, will be negative), you'll get a markedly less positive fair value, so I didn't do that.

My point is that Amkor's true value is higher than today's price, but I cannot justify today's price knowing what the company's cash flow and balance sheet will look like in the near term.

The Risks And My Concerns

In my view, the main risk to Amkor's business is how reliant it is on Apple. Apple makes up ~30% of the company's sales, and it is a single point of failure that I don't think Amkor can resolve, especially since it is now an anchor customer for the Arizona facility. We've seen how Apple behaves when it comes to bringing its operations in-house with strategically important steps. I'm talking about its M and Bionic chip designs for Macs and iPhones/iPads. Intel and Samsung used to make the chips for those devices while raking in billions every year, but that's not the case anymore.

I'm not saying that Apple will suddenly bring advanced packaging for its chips in-house, but it is possible that it shifts its sourcing strategy. Given how much of Amkor's revenue is tied to that one company, it's reasonable to say that even a small shift will shake its financials pretty hard.

Besides that, the amount of money that the company will spend on capex over the next few years isn't something to sneeze at. Yes, Amkor isn't poor, by any metric, but it still has to get the money from somewhere. I already talked about how its cash reserves and cash flow will take a hit over the next few years, but the company will also need to borrow a lot of money. That could be from its revolving credit facility and term loan, but it is possible that it has to raise additional debt. If Amkor doesn't grow revenue as quickly as we expect to cover the repayments, we're only going to see the debt become more expensive than it should be.

Then, there's the not-so-small threat of TSMC (Taiwan Semiconductor Manufacturing Company). TSMC's 3DFabric platform covers its own CoWoS (Chip on Wafer on Substrate), SoIC (System on Integrated Chips), and InFO (Integrated Fan-Out) technologies, and it competes directly with Amkor's growth engine. I know that Amkor is part of TSMC's 3DFabric Alliance, but that doesn't change the fact that some of its potential customers, like the hyperscalers, may prefer to just use TSMC's integrated foundry-plus-packaging model at source.

The Near-Term Outlook Makes It A Hold For Me

All the signs point to the fact that Amkor is a well-run company that is building the right infrastructure at the right time in today's semiconductor cycle. The tailwinds are there, and I believe in the long-term story.

What I'm less bullish about is the price, because it already reflects a base-case scenario for something whose payoff is two years away. We also have to contend with negative free cash flow and lower margins in the meantime, so it's not a good time to jump in. Having said that, I'll be more inclined to rate the stock higher if the price falls closer to the low-to-mid thirties, but no more.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

Login to comment