Some people were surprised to hear that I'm open to updating S&P Dow Jones Indices' requirements for which companies are included in the S&P 500.

I think their methodology is very good. But I wouldn't say it's perfect. Most would agree that it has its weaknesses. And admittedly, I couldn't tell you what perfect would look like.

I do know that rules are rarely perfect the first time they're written. The U.S. Constitution has been amended 27 times. The NBA regularly updates the rules of the game. Even casual fans of soccer have noticed that FIFA has introduced new rules for World Cup play. And of course, S&P Dow Jones makes changes to inclusion requirements for its many indexes.

Ultimately, I think that if we discover and agree on ways an index can better deliver on its aims, we should make changes.

Changes in methodology don't have to mean big changes to performance ⚖️

As I mentioned in Wednesday's newsletter, I'm not crazy about S&P Dow Jones' requirement for positive GAAP net income for "the most recent quarter, and the sum of the most recent four consecutive quarters." It's a backward-looking metric, and I'm in the camp that believes stocks trade largely on expectations for future profits.

SpaceX (NASDAQ:SPCX) is an example of a massive, unprofitable company that's largely trading on expectations for future profitability. Sure, there's no guarantee that it ever earns the kind of profits that justify the current valuation. Nevertheless, it's a bit odd to me to exclude such a large company from indices intended to reflect the broad market. (To be clear, this doesn't mean I think SpaceX or any other large company should be added right away. More on that here.)

That said, I also don't know if there's an elegant solution to this issue that doesn't lead to people freaking out.

I did stumble across some interesting alternatives while doing some academic reading and earning continuing education credits.

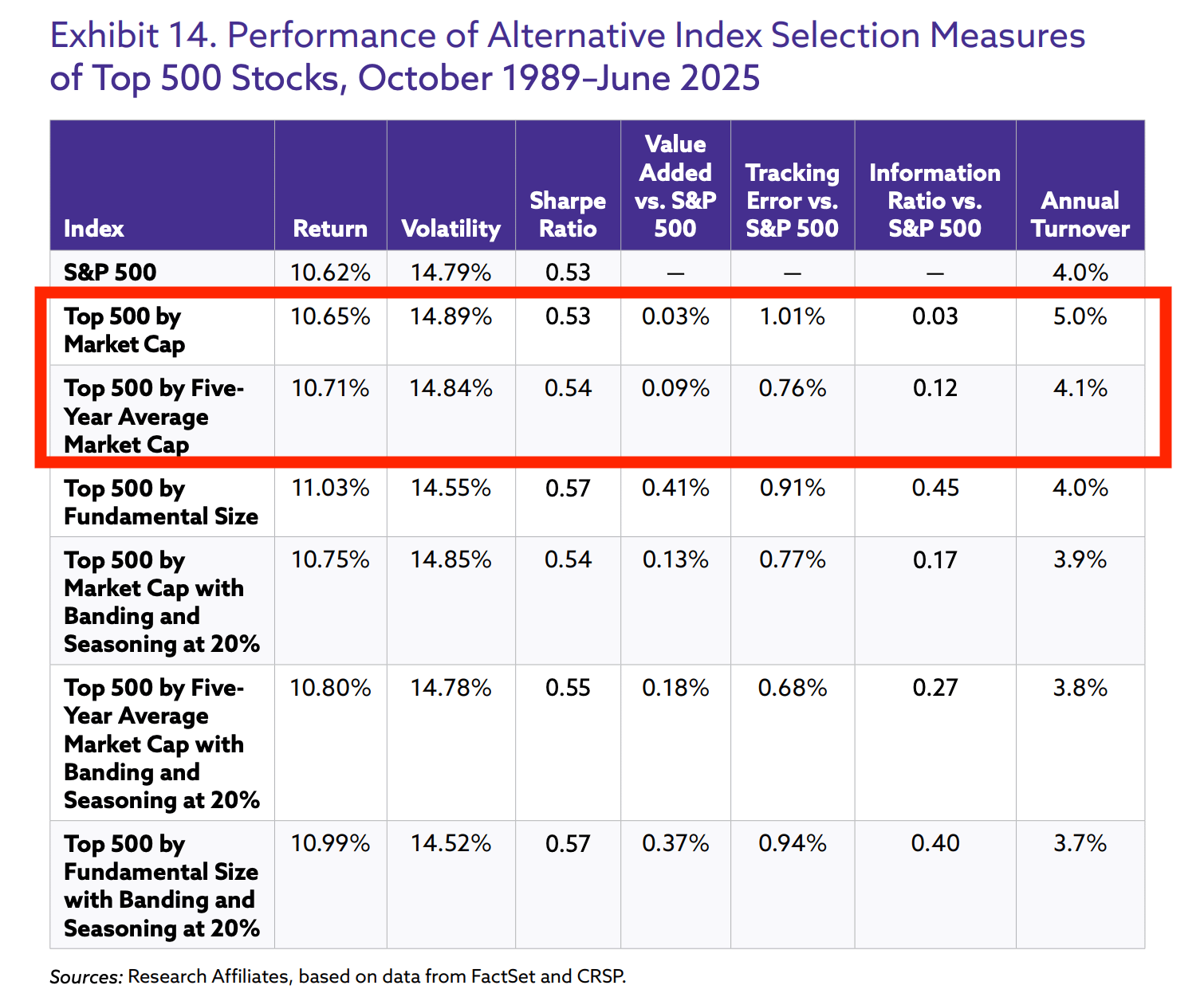

Rob Arnott and Lillian Wu recently published a paper for the CFA Institute Research & Policy Center. Titled "The Active Side of Indexing," the paper argues that despite being labeled a passive index, the S&P 500's design makes it more of an active momentum-driven, "buy high, sell low" strategy with hidden costs that cause performance to drag. It's a great read.

Among other things, they point out how the index doesn't necessarily include the 500 largest publicly traded U.S. companies.

"On average between 1991 and 2022, the index overlaps with only about 380 of the 500 largest companies in terms of market cap at any point in time," they noted. "This means that 120 of the true top 500 market-cap names are excluded, and a similar number of smaller-cap firms take their place. This discrepancy is not a trivial rounding error."

In their work, the authors explored several alternative methodologies for index construction, including simple market cap and five-year average market cap inclusion requirements. Both get around the profitability problem and other subjective judgments made by the folks at S&P Dow Jones Indices.

They tested what past performance would've looked like under these alternative approaches. Interestingly, the results weren't too dissimilar from the S&P 500's performance. In fact, the returns were slightly better.

Arnott and Wu's paper has much more, and it left me with a lot to think about. You can read it here.

I found the results of their alternative index study eye-opening. The findings suggest it's possible to make significant changes to index inclusion methodology without totally altering the performance, which may make implementing such changes more palatable for investors.

Again, I don't know what the ultimate answer is.

Maybe they keep the S&P 500 as is, but expand alternative, similar offerings that address concerns investors have regarding inclusion requirements.

Whatever happens, this debate is sure to intensify, especially as a growing number of mega-cap companies hit the market while being excluded from what are supposed to be broad market indices.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

Login to comment