Market Overview

It was another turbulent week that began with the potential for capitulation as geopolitical tensions remain high. Once again, the Nasdaq was down the least amongst the major indices, as it sold off 1.26%. The S&P 500 dropped 1.60%, while the Dow Jones Industrial Average slipped 1.99%. Energy ran the table again but tech is starting to show relative strength against the indices. Evidence points to capitulation of some form being around the corner, otherwise, something much more grave and serious is about to pan out.

Stocks I Like

IonQ (NYSE:IONQ) – 81% Return Potential

What's Happening

- IonQ, Inc. (IONQ) is a leading quantum computing company developing trapped-ion quantum systems and software for high-performance computations, offering cloud-based access through major platforms like AWS, Azure, and Google Cloud, providing investors exposure to the rapidly growing quantum technology and advanced computing sector with a focus on scalable, error-corrected quantum solutions for AI, optimization, and scientific applications.

- The company reported revenue of $61.89 million but no earnings in the last quarter.

- The valuation in IONQ is steep. Price-to-Sales is at 77.34 and Book Value is just 10.36.

- From a technical standpoint, IONQ is pulling back into a channel after gapping higher. If a higher-low forms here, it would signal the tide is turning bullish again.

Why It's Happening

- IonQ Inc. is spearheading the quantum computing revolution with its trapped-ion technology, achieving industry-leading gate fidelities and system scale that enable practical applications in drug discovery, optimization, and cryptography. As quantum systems transition from labs to real-world problem-solving, IonQ’s hardware is positioned to capture early commercial wins in a market projected to reach trillions in value, creating a transformative story for computing’s future.

- Rapid revenue acceleration underscores IonQ’s maturation from R&D to commercialization, with triple-digit annual growth pushing sales past $100 million in 2025 and on track for further doubling by 2026. This momentum reflects deepening enterprise adoption for quantum simulations and algorithms, building a flywheel of recurring contracts that solidifies IonQ as a foundational player in the emerging quantum economy.

- Strategic focus on quantum advantage sets IonQ apart in solving classically intractable problems, with its roadmap targeting error-corrected systems by 2026 that could revolutionize industries like materials science and finance. By prioritizing scalable, high-performance qubits over competitors’ approaches, IonQ is crafting a narrative of pioneering breakthroughs that unlock unprecedented computational power for global challenges.

- Diversified ecosystem partnerships enhance IonQ’s growth potential, collaborating with cloud providers and research institutions to integrate quantum access into existing workflows. This open-platform strategy democratizes quantum tech, fostering widespread innovation and positioning IonQ to benefit from the network effects of an expanding developer community in a nascent but explosive field.

- Exposure to national security and AI synergies amplifies IonQ’s long-term vision, as quantum computing complements AI in hybrid models for advanced simulations and secure communications. With increasing government investments in quantum resilience amid geopolitical tensions, IonQ’s U.S.-based operations create a compelling story of strategic importance and sustained demand in defense and tech sectors.

- IONQ is a candidate for a short squeeze with over 22% of the stock being sold short.

- Analyst Ratings:

- Benchmark: Buy

- Goldman Sachs: Neutral

- Craig-Hallum: Buy

My Action Plan (81% Return Potential)

- I am bullish on IONQ above $30.00-$31.00. My upside target is $78.00-$80.00.

Bullish (NYSE:BLSH) – 31% Return Potential

What's Happening

- Bullish (BLSH) is a leading digital asset platform providing market infrastructure and information services, operating the Bullish Exchange for spot and derivatives trading in cryptocurrencies while offering indices, data analytics, and media insights through CoinDesk, providing investors exposure to the rapidly growing blockchain and digital finance sector with a focus on institutional liquidity, benchmarks, and innovative market solutions.

- The last quarterly report showed revenue of $92.5 million and earnings of $28.86 million.

- Valuation is decent in BLSH. Price-to-Sales is just 0.02 and Book Value is at 21.42.

- From a technical point of view, BLSH is on the verge of confirming a low by breaking out from a rounding bottom formation. This could lead to an explosive rally higher.

Why It's Happening

- Bullish is spearheading institutional adoption of digital assets, with its platform facilitating over $1.25 trillion in cumulative trading volume and managing $2 billion in cryptocurrency assets, primarily Bitcoin and Ethereum. This focus on high-value institutional clients creates a stable revenue base less susceptible to retail volatility, positioning the company to thrive as regulatory clarity and ETF approvals draw more traditional finance into crypto.

- Rapid revenue diversification through CoinDesk’s subscriptions, indices, and data services provides recurring income streams beyond trading, with recent quarters showing 72% year-over-year growth to $76.5 million. This balanced portfolio, including market analytics and insights, enhances resilience and taps into the growing demand for reliable crypto intelligence in a maturing digital economy.

- Strategic U.S. market entry via a BitLicense unlocks vast new opportunities for Bullish, enabling operations in one of the world’s largest financial hubs and attracting institutional investors seeking compliant, secure platforms. This expansion, coupled with international growth, builds a global footprint that capitalizes on rising cross-border crypto flows and institutional interest.

- Launch of derivatives and liquidity services doubles down on Bullish’s institutional edge, with partnerships surging 50% sequentially and driving net income from prior losses to $18.5 million. These high-margin offerings address sophisticated trading needs, fostering deeper client relationships and positioning the company as a comprehensive solution in the evolving crypto infrastructure landscape.

- Experienced leadership from ex-NYSE executives steers Bullish toward bridging traditional finance and crypto, founded in 2020 with a vision to create robust market infrastructure. This expertise, combined with a debt-free balance sheet post-IPO, supports aggressive innovation and scalability, making Bullish a pivotal player in the trillion-dollar potential of institutional crypto markets.

- BLSH is a candidate for a short squeeze with over 18% of its floated shares being sold short.

- Analyst Ratings:

- JP Morgan: Neutral

- Rosenblatt: Buy

- Citigroup: Buy

My Action Plan (31% Return Potential)

- I am bullish on BLSH above $31.00-$32.00. My upside target is $49.00-$50.00.

FreshPet (NASDAQ:FRPT) – 63% Return Potential

What's Happening

- Freshpet, Inc. (FRPT) is a leading manufacturer of natural fresh meals and treats for dogs and cats, distributing premium pet food through innovative company-owned refrigerated displays in grocery, mass, club, pet specialty, and natural stores across North America and Europe, offering investors exposure to the rapidly growing pet care and consumer staples sector with a focus on health-conscious nutrition and sustainable ingredients.

- The company's latest quarterly report showed revenue of $285.23 million and earnings of $34.48 million.

- Valuation in FRPT is a bit high. P/E is at 31.37, Price-to-Sales is at 4.21, and EV to EBITDA is at 24.51.

- From a charting standpoint, FRPT has built a massive saucer formation, which points to tremendous gains on the horizon.

Why It's Happening

- Freshpet Inc. is capitalizing on the premium pet food boom with its fresh, refrigerated products driving record 2025 sales of $1.1 billion, up 13% year-over-year, fueled by expanding household penetration and store distribution. This momentum positions the company to sustain growth into 2026 with guided net sales increases of 7-10%, reflecting its ability to meet rising consumer demand for high-quality, natural nutrition amid a shift toward humanizing pet care.

- Operational excellence and margin expansion are transforming Freshpet’s profitability story, achieving positive free cash flow and record net income of $139 million in 2025 through efficient capacity utilization and cost discipline. This financial turnaround enables reinvestment in innovation and expansion, creating a resilient foundation for continued earnings growth as the company scales its fresh pet food ecosystem in a market hungry for premium alternatives.

- Strategic focus on product innovation enhances Freshpet’s market dominance, with new launches in skin health and weight management supplements complementing its core refrigerated offerings to address evolving pet owner needs. This diversified portfolio taps into the broader wellness trend, fostering customer loyalty and recurring purchases while positioning Freshpet as an indispensable brand in the growing $50 billion+ pet food industry.

- Global and regional expansion opportunities support Freshpet’s long-term vision, leveraging its U.S. leadership to explore international markets where demand for premium pet products is accelerating. With a proven model of store growth and consumer adoption, the company is well-equipped to navigate economic cycles, building a sustainable narrative of geographic diversification and market share gains in underserved areas.

- Commitment to sustainability and quality resonates with health-conscious consumers, as Freshpet’s use of responsibly sourced ingredients aligns with broader ESG trends in pet care. This focus not only differentiates the brand in a competitive landscape but also drives premium pricing power and brand equity, reinforcing its story as a forward-thinking leader poised for enduring success in the evolving pet wellness sector.

- The stock could experience a modest short squeeze as +14% of its floated shares are being sold short.

- Analyst Ratings:

- DA Davidson: Buy

- Wells Fargo: Overweight

- JP Morgan: Neutral

My Action Plan (63% Return Potential)

- I am bullish on FRPT above $68.00-$70.00. My upside target is $125.00-$130.00.

Market-Moving Catalysts for the Week Ahead

The Danger of Fear-Based Trading

There's a lot to be concerned about in the world right now. There are two major geopolitical conflicts going on in Iran and Ukraine, oil prices are skyrocketing, and stock markets are trading on edge.

Fear is in the air. It's not quite a full-blown panic, but it doesn't need to be. If stocks have bottomed, people now have a reason to be skeptical of stocks going higher – this is exactly what's needed to create a sustainable bull trend.

It may not sound very nice, and it's not. Markets aren't here to make everyone feel warm and fuzzy. Trade the headlines at your own peril – you need to have technical levels and tight risk-reward considerations to trade this environment.

K-Shaped Economy Accelerating

The K-shaped economy, characterized by divergent recoveries where high-income individuals and sectors thrive while low-income groups and industries lag, will only accelerate due to spiking crude oil prices and their inflationary ripple effects.

Surging oil costs drive up transportation, manufacturing, and energy expenses, inflating prices for essentials like fuel, food, and utilities, which disproportionately burden lower-wage earners who spend a larger share of their income on necessities and have limited savings to cushion the blow.

Meanwhile, wealthier households and asset-heavy sectors, such as energy producers or investors in commodities, may benefit from higher profits or portfolio gains, widening the inequality gap. This dynamic makes economic mobility even harder, as struggling small businesses and service industries face higher operational costs without corresponding revenue growth, potentially leading to job losses and prolonged stagnation for the downward arm of the “K.” Remember this if stocks go up – it only benefits those that actually own them.

Sector & Industry Strength

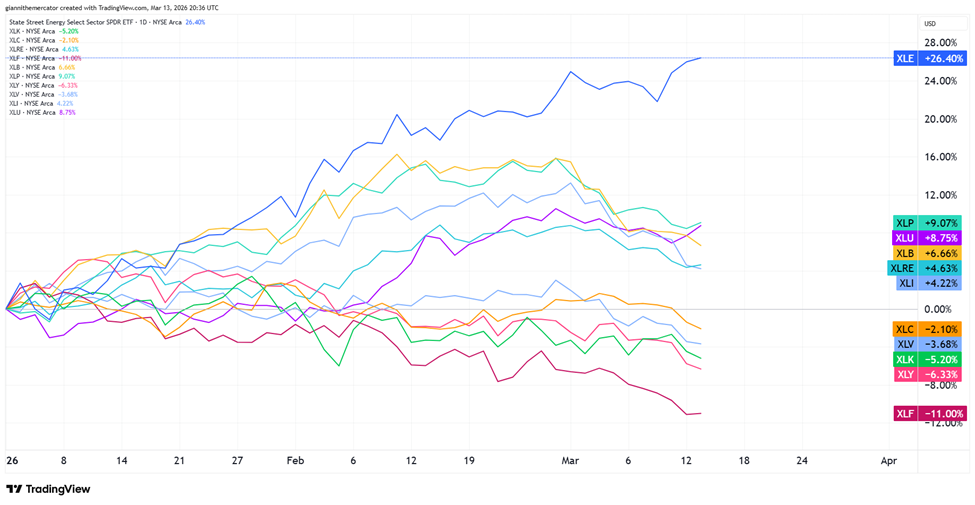

Since we're coming down to the wire of the first quarter, I want to tighten up the timeframe on the sector stack to see if there's anything else hiding under the surface. Unfortunately for bulls, there is still more money flows into defensive areas of the market than growth.

Of course, this can flip quickly and we'll see growth start to rebound first at the short-term interval before anything else. The most ominous observation in this tape is how financials (XLF) are being utterly obliterated – they're the 2nd largest sector in the S&P.

Energy (XLE) remains by far and away the strongest sector year-to-date, with utilities coming in second. This is not what bulls want to see. Bulls need to see a strong rebound in growth sectors like tech (XLK), communications (XLC), and consumer discretionary (XLY) sooner than later.

| 1 week | 3 Weeks | 13 Weeks | 26 Weeks |

| Energy | Energy | Energy | Energy |

Editor's Note: The inflationary flush continues.

What's Next for Energy? (Sector ETF: XLE/SPY)

One of the most notable observations last week in light of the recent surge in oil prices was how the energy sector (XLE) didn't see similar gains. This begs the question – was this an exhaustion move or does the market not fully appreciate what's going on?

I'm looking at the ratio between the energy sector (XLE) and the S&P 500 (SPY). The energy sector lagged the broader market for years – basically from October 2022 to December 2025. The ratio experienced a powerful surge in favor of energy since the end of last year.

But this chart is at a key inflection point now. It made a slightly higher-high above 2025's high, which is encouraging for bulls, but within the greater trend, this could end up being a lower-high too. I'm also watching the wedge pattern here closely because if prices clear resistance, then energy will be a great place to be overweight for the rest of 2026.

Ignore the Noise – Focus on Chips (Sector ETF: SMH/QQQ)

The fog of war is a real phenomenon, but at the end of the day, we're trading the price action in the market, and the capital flows are still pointing in a direction that favors the bullish case in time.

It's time to check back in on the most important market ratio for this bull market – this chart shows semiconductors (SMH) relative to the Nasdaq 100 (QQQ). This is a ratio that has defined the AI theme over the past few years. In other words, no chips, no party.

The ratio remains in a strong, steady uptrend. It has been completely undeterred by the recent geopolitical events, which means a lot of it could just be noise. It's been accelerating ever since the breakout from the wedge, and as long as it continues higher, there's not going to be a bear market.

The Bond Read on Inflation (Sector ETF: TIP/IEF)

For all the fuss about inflation spiking right now, bonds don't actually seem that concerned. It may sound counterintuitive, but at the end of the day, we're not seeing a big spike in inflation-sensitive areas of the bond market.

I have the ratio here between Treasury Inflation Protected Securities (TIP) and 7-10 Year Treasuries (IEF). The idea here is that TIP will outperform IEF when inflation expectations are rising, as the interest rate on those types of Treasuries adapts to CPI data.

While there was a notable spike in this ratio in late-February, it's been rather tame given the price action of crude oil. It would seem that bonds think this oil spike may be temporary. Plus, it hasn't made a significant higher-high, nor has it resolved from the symmetrical triangle formation – it remains range bond for now, which means inflation may stay contained.

Cryptocurrency

Back to Bitcoin this week. I must admit I am pleasantly surprised at the resilience it's displayed in this volatile environment. The trend remains in favor of the bears, although we cannot fully dismiss a higher-low being complete last week.

Bigger picture, it's still consolidating its losses into a bear flag or even a rectangle pattern. This leaves the door open for a final flush lower, with downside targets at 53,000-56,000 and even 40,000-45,000 remaining intact.

However, if prices take out the March 4 high at 74,075, it would create a higher-high, and put the bears in a rather uncomfortable position. It would still need to get back above 84,000-86,000 to entertain the idea that a significant low is complete.

Legal Disclosures:

This communication is provided for information purposes only.

This communication has been prepared based upon information, including market prices, data and other information, from sources believed to be reliable, but Benzinga does not warrant its completeness or accuracy except with respect to any disclosures relative to Benzinga and/or its affiliates and an analyst’s involvement with any company (or security, other financial product or other asset class) that may be the subject of this communication. Any opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This communication is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Benzinga does not provide individually tailored investment advice. Any opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. You must make your own independent decisions regarding any securities, financial instruments or strategies mentioned or related to the information herein. Periodic updates may be provided on companies, issuers or industries based on specific developments or announcements, market conditions or any other publicly available information. However, Benzinga may be restricted from updating information contained in this communication for regulatory or other reasons. Clients should contact analysts and execute transactions through a Benzinga subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

This communication may not be redistributed or retransmitted, in whole or in part, or in any form or manner, without the express written consent of Benzinga. Any unauthorized use or disclosure is prohibited. Receipt and review of this information constitutes your agreement not to redistribute or retransmit the contents and information contained in this communication without first obtaining express permission from an authorized officer of Benzinga. Copyright 2022 Benzinga. All rights reserved.

Login to comment