Editor’s note: This article was updated to add more detail and context.

The Federal Reserve’s preferred inflation gauge climbed again in May as the energy shock continued to filter through the broader consumer basket, the Bureau of Economic Analysis reported Thursday.

The headline Personal Consumption Expenditure price index rose 0.4% on the month, missing the 0.5% expected after April’s 0.4% gain.

From a year earlier, it quickened from 3.8% to 4.1%, matching the 4.1% forecast and marking the highest reading since April 2023.

Core PCE, which strips out food and energy, rose 0.3% on the month, matching both the previous and expected 0.3%.-

The annual rate inched up from 3.3% to 3.4%, matching estimates.

The report marks the third straight uncomfortable inflation print to land on the desk of new Fed Chair Kevin Warsh, bolstering investor bets on interest-rate increases.

Money markets now price a near-certain 25-basis-point hike in the fed funds rate by October 2026, with a second increase expected by March 2027.

Inflation Rises But US Consumers Keep Spending

The May Personal Income and Outlays report pointed to resilient consumers.

Personal income rose 0.7% on the month — its strongest gain since July 2025 and well above the 0.4% consensus — while personal spending also climbed 0.7%, or $156.1 billion, beating estimates of 0.6% and accelerating from a downwardly revised 0.4% in April.

The spending gain was broad-based, with outlays rising $94.3 billion on services and $61.8 billion on goods. Adjusted for inflation, real consumer spending increased 0.3% in May after a flat reading in April.

The strength in demand, set against a 0.4% rise in prices, suggests households are still spending even as the cost of living keeps climbing.

A Stronger Q1 GDP Print

In a separate release, the BEA’s third estimate showed the US economy grew at a 2.1% annualized rate in the first quarter, revised up from the 1.6% second estimate and a sharp acceleration from 0.5% in the fourth quarter of 2025.

The upgrade, however, was not driven by stronger domestic demand. It reflected almost entirely a downward revision to imports — which subtract from GDP — partly offset by a downward revision to consumer spending.

Final first-quarter real consumer spending was cut to 0.5% from prior estimates, and real final sales to private domestic purchasers, a cleaner gauge of underlying demand, was revised down to 1.7%.

The GDP report’s quarterly inflation gauges underscored the price pressure: the PCE price index rose 4.6% in Q1 and the core measure 4.4%. Corporate profits from current production increased $74.4 billion, revised up $34 billion.

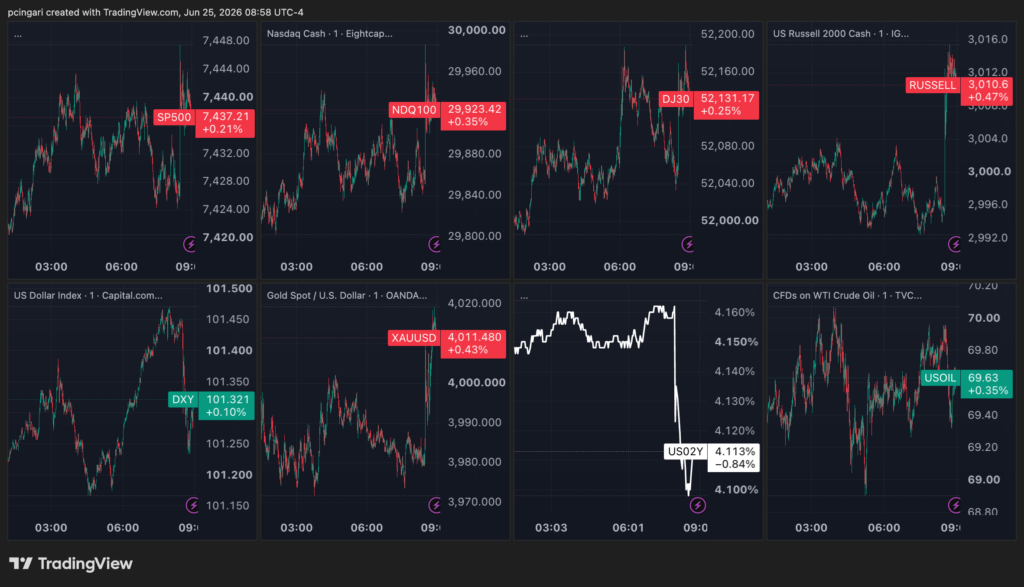

Market Reaction: Relief Across The Board

Equities pushed higher after the in-line inflation data.

Futures on the S&P 500 were up 0.2% to 7,450 points, while contracts on the Nasdaq 100 rose 0.4%

Small caps led the move, with the iShares Russell 2000 ETF (NYSE:IWM) up around 0.5% in the premarket as the rate-sensitive corner of the market cheered the expected print.

The Treasury market did the heavy lifting. The policy-sensitive 2-year yield fell about 5 basis points to 4.10%, as traders trimmed bets on a near-term hike.

The dollar slipped from the one-year high it reached earlier in the session, with the US Dollar Index easing back toward 101.27.

Gold rebounded above $4,000 an ounce, rising about 0.5% after a brutal stretch that had dragged bullion to an eight-month low.

Crude oil remained under heavy pressure, with West Texas Intermediate trading below $70 a barrel as the reopening of the Strait of Hormuz unwound the war-risk premium that had driven prices higher during the Iran conflict.

Image: Shutterstock

Login to comment