Nikola Corporation (OTC:NKLAQ) was once one of Wall Street’s most closely watched electric-vehicle startups. After going public through a SPAC merger in 2020, the hydrogen-truck developer briefly reached a valuation of nearly $30 billion—despite having little commercial revenue and no proven path to profitability.

That optimism collapsed after questions emerged about Nikola’s technology, production capabilities, and business prospects. The controversy led to regulatory investigations, founder Trevor Milton’s resignation and fraud conviction, years of investor litigation, and a near-total loss of shareholder value.

Nikola filed for Chapter 11 bankruptcy in February 2025 with approximately $47 million in cash. Its assets were subsequently placed into a court-supervised sale process, and its liquidation plan provided for the cancellation of common shares without a distribution to equity holders.

Meanwhile, the investor securities class action has entered the settlement stage. The parties have reached an agreement in principle, although the final amount and distribution terms are still being negotiated and will require court approval.

From EV Growth to Investor Litigation

Nikola presented investors with an ambitious plan to produce battery-electric and hydrogen fuel-cell trucks while developing the fueling network required to support them.

The company promoted its vehicle technology, planned production capacity, commercial partnerships, and thousands of potential truck orders. The lawsuit alleges that several of those statements overstated Nikola’s technological readiness, in-house capabilities, production progress, and commercial prospects.

The defendants have denied wrongdoing. Separately, Nikola previously agreed to resolve an SEC enforcement action, while Milton was convicted on fraud-related charges arising from statements about the company’s products and operations.

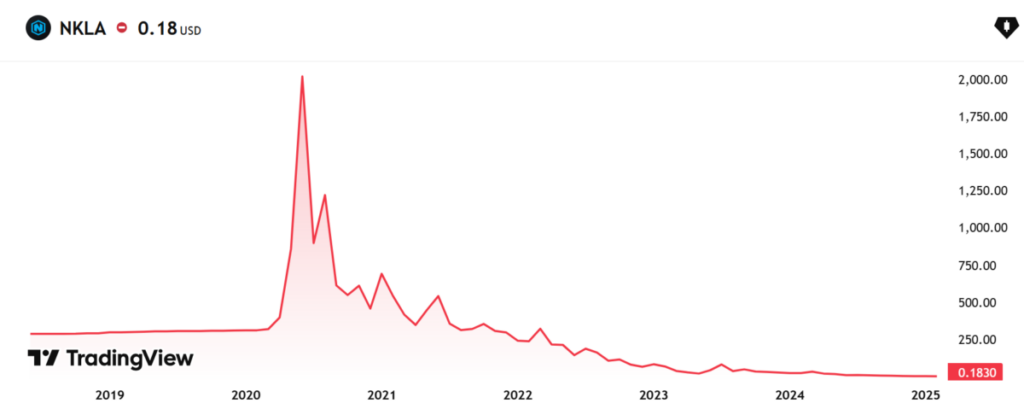

As concerns became public, investor confidence disappeared. Nikola’s stock entered a prolonged decline that eventually erased nearly all of its value.

How Nikola’s Stock Broke Down

Nikola’s stock followed a pattern often seen in highly speculative growth companies.

During its early public-market phase, the shares were driven more by expected market potential than by current financial performance. Investors priced in the possibility that Nikola could become a major player in zero-emission trucking before the company had demonstrated meaningful production, recurring revenue, or positive cash flow.

Once the credibility of management’s claims came under scrutiny, that momentum reversed. Large selloffs were followed by weaker rebounds, lower highs, and repeated moves to new lows. Instead of building a stable technical base, the stock continued to lose support.

Repeated share issuance and reverse stock splits added further pressure. Reverse splits increased the quoted price per share but did not restore Nikola’s market value or improve its underlying economics. Each additional financing also diluted existing shareholders.

By early 2025, Nikola’s chart no longer reflected a temporary correction. It reflected a market that had largely abandoned the turnaround thesis. The stock dropped roughly 40% following the bankruptcy announcement, after already losing nearly all of its value from its 2020 peak.

Once trading was suspended and the liquidation plan called for the cancellation of common stock, traditional technical indicators became largely irrelevant.

How Nikola’s Financial Position Deteriorated

Nikola’s central problem was the gap between the cost of its strategy and the revenue produced by the business.

Developing commercial trucks is capital-intensive. Building a hydrogen-fueling network at the same time made the model even more expensive. Nikola had to fund manufacturing, engineering, vehicle support, infrastructure, and continued product development before it had enough customers or production volume to absorb those costs.

Although Nikola eventually delivered battery-electric and fuel-cell trucks, its volumes remained too low to support the business. In the third quarter of 2024, it produced 83 trucks while recording a net loss of almost $200 million.

The company was therefore dependent on continuous external financing. But as its stock price fell and investor trust weakened, raising capital became increasingly expensive and dilutive.

Nikola also accumulated significant debt while continuing to burn cash. Before bankruptcy, reports indicated that it was consuming approximately $150 million per quarter and had not generated positive free cash flow.

By February 2025, its remaining $47 million cash balance was insufficient to support a credible long-term turnaround. The company could fund only limited operations while seeking buyers for its assets.

What the Settlement Means for Investors

The securities class action now provides a potential recovery path for eligible investors.

The parties have reached an agreement in principle, although the final settlement amount, class eligibility, loss calculations, and claims process are still being negotiated and will require court approval.

Even after approval, payments would not be automatic. Eligible investors would need to submit a valid claim supported by their Nikola trading records and meet the final filing requirements.

For former shareholders, the settlement may therefore represent one of the few remaining opportunities to recover a portion of their losses.

Current Market Sentiment

Market sentiment toward Nikola is no longer simply bearish. The original equity story has effectively ended.

Before bankruptcy, investors could still speculate that Nikola might reduce costs, raise additional capital, secure a strategic partner, or scale hydrogen-truck deliveries. The confirmed liquidation plan largely removed those possibilities for common shareholders.

Nikola’s equipment, technology, intellectual property, and engineering assets may still have value to other companies. However, value created through asset sales is distributed according to bankruptcy priorities, with creditors paid before shareholders.

That does not necessarily mean hydrogen trucking has no future. Fuel-cell vehicles may still have applications in long-distance commercial transport where range and refueling speed matter. But the market is likely to demand stronger balance sheets, proven demand, functioning infrastructure, and credible production economics before assigning premium valuations to the next generation of hydrogen companies.

What Happens Next?

Nikola is expected to continue primarily as a legal and administrative estate while asset sales, creditor distributions, and remaining litigation are completed. For common shareholders, a recovery through the bankruptcy process is highly unlikely because the liquidation plan cancels the equity without a distribution.

For creditors, recoveries will depend on the final value of Nikola’s assets, the priority of individual claims, and the cost of administering the bankruptcy.

For investors included in the securities class action, partial recovery remains possible. However, the final settlement terms must still be negotiated, documented, and approved by the court before a formal claims and distribution process can begin.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

Login to comment